No matter how the housing market changes, there are some things about owning a home that never change—like the personal benefits it can provide. When you own your home, you likely feel a sense of attachment because of the comfort it gives and also because it’s a space that’s truly yours.

Over the last few years, we’ve fully embraced the meaning of our homes as we spent more time than ever in them. As a result, the emotional benefits our homes provide have become even more important to us.

“. . . one thing has stayed the same: the home continues to be of the utmost importance and a place of security and comfort.”

The same study from Unison notes:

91% of homeowners say they feel secure, stable, or successful owning a home

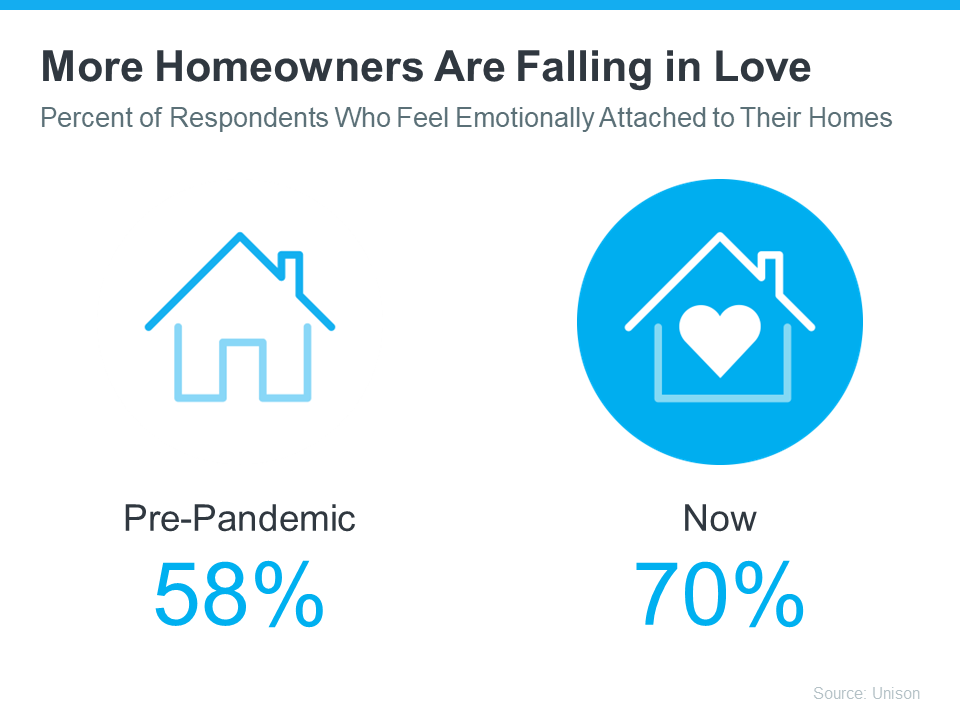

64% of American homeowners say living through a pandemic has made their home more important to them than ever

It’s no surprise this study also reveals that homeowners now love their homes even more as our attachments to them have grown:

The National Association of Realtors (NAR) also explains:

“In addition to tangible financial benefits, homeownership brings substantial social benefits for [households], communities, and the country as a whole.”

In other words, not only does owning a home build your net worth over time, but it also gives you and your loved ones a place to thrive. And by living near people with shared experiences, homeownership helps you connect with your community and contribute meaningfully.

Bottom Line

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, let me be the key to unlocking a home you can truly fall in love with.

Before you buy a home, it’s important to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home, you need to understand what closing costs are and how much you should budget for.

What Are Closing Costs?

People are sometimes surprised by closing costs because they don’t know what they are. According to Bankrate:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”

In other words, your closing costs are a collection of fees and payments involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

Government recording costs

Appraisal fees

Credit report fees

Lender origination fees

Title services

Tax service fees

Survey fees

Attorney fees

Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical, too. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $366,900. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $7,500 and $18,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared at Closing Time?

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

Work with a team of trusted real estate professionals to understand exactly how much you’ll need to budget for closing costs. An agent can help connect you with a lender, and together your expert team can answer any questions you might have.

Bottom Line

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process.

New Homes May Have the Incentives You’re Looking for Today

According to the U.S. Census Bureau, this year, builders are on pace to complete more than a million new homes in this country. If you’ve had trouble finding a home to buy over the past year, it may be time to work with your trusted agent to consider a new build and the incentives that come with it. Here’s why.

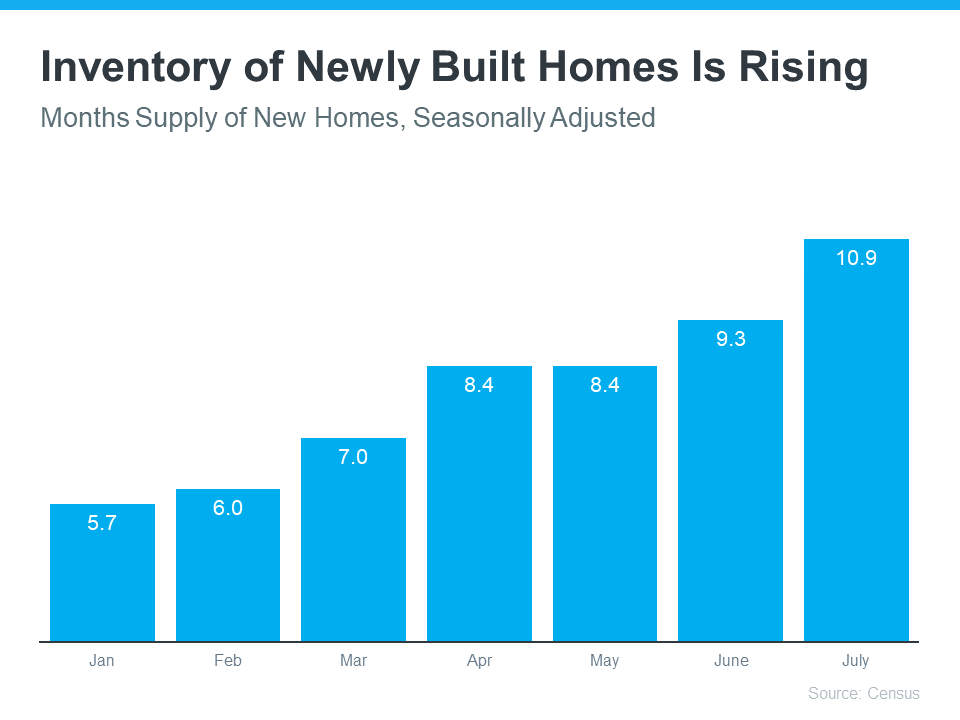

The Supply of Newly Built Homes Is Rising

When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the inventory of existing homes is on the rise today, it’s still in tight supply, meaning it can be challenging to find just the right one.

The inventory of newly built homes, however, is also rising. And with more options available than there have been in years, a new home may be just the answer you’re looking for. The graph below shows just how much the supply of newly built homes has grown this year.

And here’s the thing – builders are also keeping a close eye on current market trends. With mortgage rates rising this year and, as a result, buyer demand softening, builders are slowing their pace of new construction. That’s because they learned their lesson in the housing crash of 2008 and want to avoid over-building and having too much inventory in their pipeline.

Basically, while there are more newly built homes on the market today than there have been in years, many builders want to sell their current inventory before adding much more – and that’s where you can really benefit. Today, builders may be more willing to work with buyers. According to a recent survey, 83% of builders have reduced their prices over the last three months.

What That Means for You

The current supply of newly built homes for sale coupled with the fact that data shows the majority of builders are doing price reductions are both great news for you. It means you may have more options and possibly some much-needed relief if you consider newly built homes in your search.

Bottom Line

If you’re ready to buy, it may be time to look for a newly built home. To learn what’s available in our area and what incentives these builders are offering, let’s connect today.

If you’re thinking about buying a home, you likely have a lot of factors on your mind. You’re weighing your own needs against higher mortgage rates, today’s home prices, and more to try to decide if you want to jump into the market. While some buyers may wait things out, there’s a reason serious buyers are making moves right now, and that’s the growing number of homes for sale.

So far this year, housing inventory has been increasing and that’s making the prospect of finding your dream home less difficult. While there are always reasons you could delay making a big decision, there are also always reasons to consider moving forward. And having a growing number of options for your home search may be exactly what you needed to feel more confident in making a move.

What’s Causing Housing Inventory To Grow?

As new data comes out, we’re getting an updated picture of why housing supply is increasing so much this year. As Bill McBride, Author of Calculated Risk, explains:

“We are seeing a significant change in inventory, but no pickup in new listings. Most of the increase in inventory so far has been due to softer demand – likely because of higher mortgage rates.”

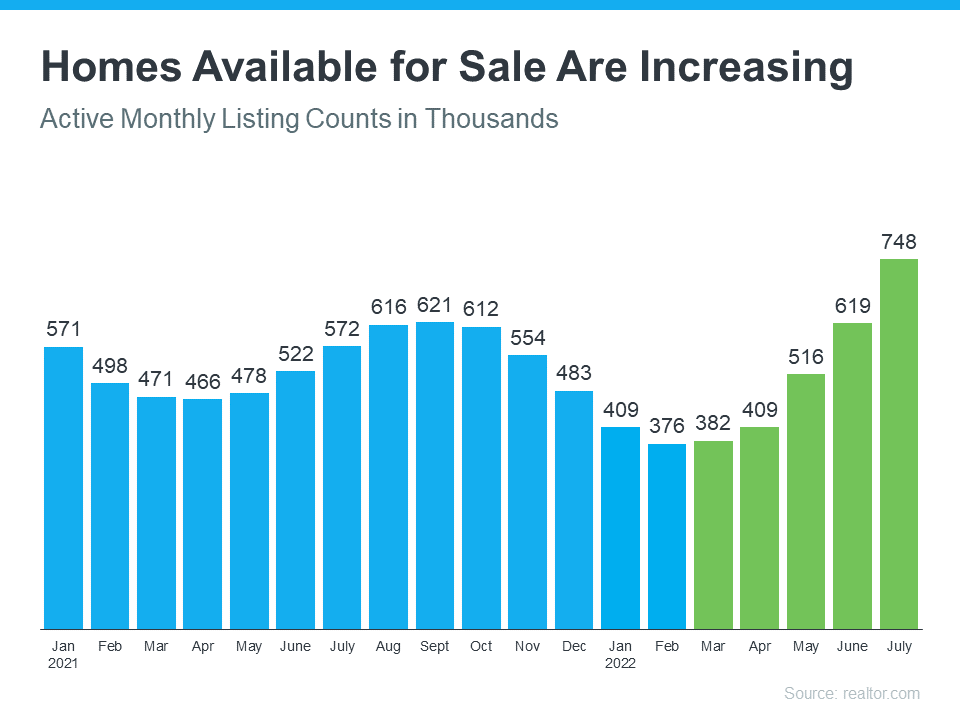

Basically, the inventory growth is primarily from homes staying on the market a bit longer (known as active listings). And that’s happening because higher mortgage rates and home prices have helped moderate the peak frenzy of buyer demand.

The graph below uses data from realtor.com to show how much active listings have risen over the past five months as a result (shown in green):

Why This Growth Is Good News for You

Regardless of the source, the increase in available housing supply is good for buyers. More housing supply actively for sale means you have more options as your search for your next home. A recent article from realtor.com explains just how significant the inventory growth has been and why it’s good news for your plans to buy:

“Nationally, the inventory of homes actively for sale on a typical day in July increased by30.7% over the past year, the largest increase in inventory in the data history and higher than last month’s growth rate of 18.7% which was itself record-breaking. This amounted to 176,000 more homes actively for sale on a typical day in July compared to the previous year and more choice for buyers who are still looking for a new home.”

The growth this year is certainly good news for you, especially if you’ve had trouble finding a home that meets your needs. If you start your search today, those additional options should make it less difficult to find a home than it would have been over the past two years.

Bottom Line

If you’re ready to jump into the market and take advantage of the increasing supply of homes for sale, let’s connect today. The opportunity is knocking, will you answer?

Why Today’s Housing Inventory Proves the Market Isn’t Headed for a Crash

Whether or not you owned a home in 2008, you likely remember the housing crash that took place back then. And news about an economic slowdown happening today may bring all those concerns back to the surface. While those feelings are understandable, data can help reassure you the situation today is nothing like it was in 2008.

One of the key reasons why the market won’t crash this time is the current undersupply of inventory. Housing supply comes from three key places:

Current homeowners putting their homes up for sale

Newly built homes coming onto the market

Distressed properties (short sales or foreclosures)

For the market to crash, you’d have to make a case for an oversupply of inventory headed to the market, and the numbers just don’t support that. So, here’s a deeper look at where inventory is coming from today to help prove why the housing market isn’t headed for a crash.

Current Homeowners Putting Their Homes Up for Sale

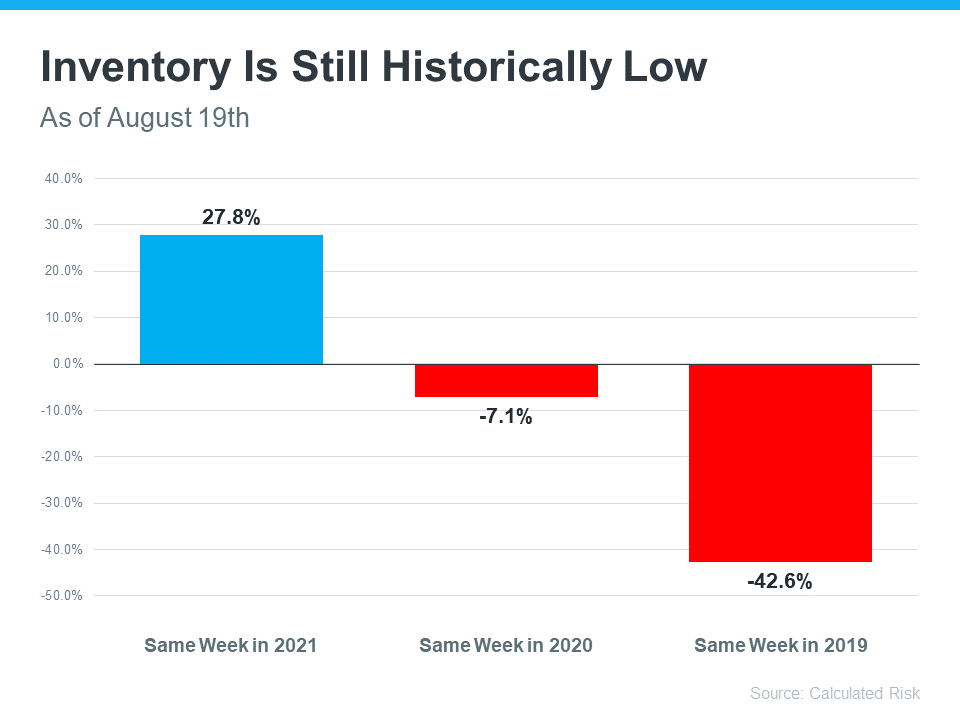

Even though housing supply is increasing this year, there’s still a limited number of existing homes available. The graph below helps illustrate this point. Based on the latest weekly data, inventory is up 27.8% compared to the same week last year (shown in blue). But compared to the same week in 2019 (shown in the larger red bar), it’s still down by 42.6%.

So, what does this mean? Inventory is still historically low. There simply aren’t enough homes on the market to cause prices to crash. There would need to be a flood of people getting ready to sell their houses in order to tip the scales toward a buyers’ market. And that level of activity simply isn’t there.

Newly Built Homes Coming onto the Market

There’s also a lot of talk about what’s happening with newly built homes today, and that may make you wonder if we’re overbuilding. But home builders are actually slowing down their production right now. Ali Wolf, Chief Economist at Zonda, notes:

“It has become a very competitive market for builders where they are trying to offload any standing inventory.”

To avoid repeating the overbuilding that happened leading up to the housing crisis, builders are reacting to higher mortgage rates and softening buyer demand by slowing down their work. It’s a sign they’re being intentional about not overbuilding homes like they did during the bubble.

And according to the latest data from the U.S. Census, at today’s current pace, we’re headed to build a seasonally adjusted annual rate of about 1.4 million homes this year. While this will add more inventory to the market, it’s not on pace to create an oversupply because builders today are more cautious than the last time when they built more homes than the market could absorb.

Distressed Properties (Short Sales or Foreclosures)

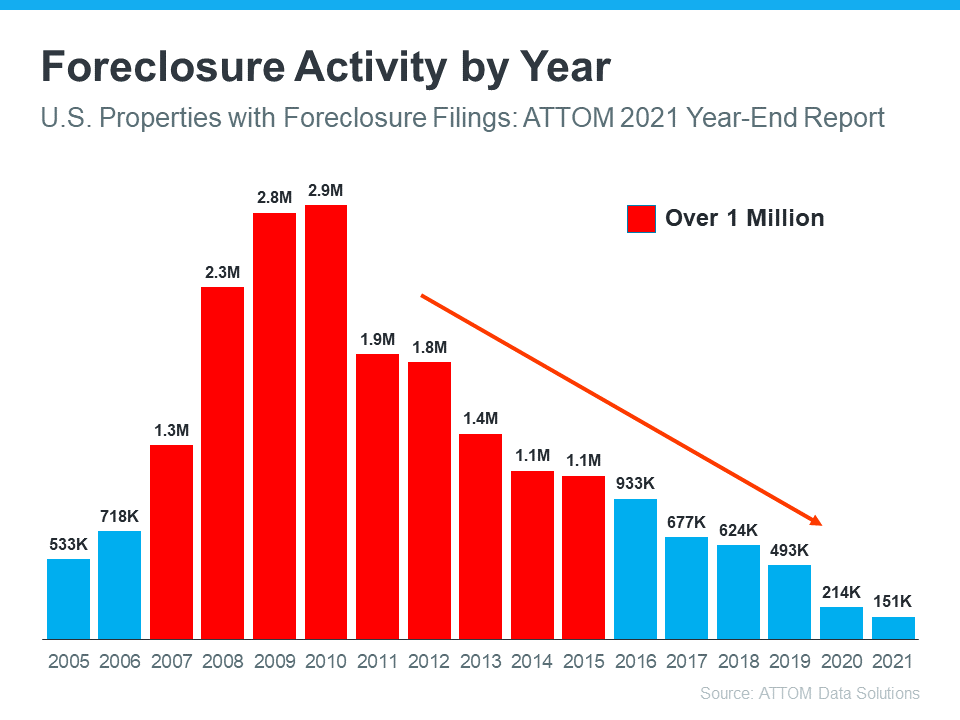

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back in the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to secure a home loan they couldn’t truly afford. Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from ATTOM Data Solutions on properties with foreclosure filings to help paint the picture of how things have changed since the crash:

This graph shows how in the time around the housing crash there were over one million foreclosure filings per year. As lending standards tightened since then, the activity started to decline. And in 2020 and 2021, the forbearance program was a further aid to help prevent a repeat of the wave of foreclosures we saw back around 2008.

That program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

Bottom Line

Although housing supply is growing this year, the market certainly isn’t anywhere near the inventory levels that would cause prices to drop significantly. That’s why inventory tells us the housing market won’t crash.

Will Home Prices Fall This Year? Here’s What Experts Say.

Many people are wondering: will home prices fall this year? Whether you’re a potential homebuyer, seller, or both, the answer to this question matters for you. Let’s break down what’s happening with home prices, where experts say they’re headed, and how this impacts your homeownership goals.

“Price appreciation averaged 15% for the full year of 2021, up from the 2020 full year average of 6%.”

So why are prices climbing so much? It’s because there are more buyers than there are homes for sale. This imbalance is expected to maintain that upward pressure on home prices because homes for sale are a hot commodity in today’s low-inventory housing market.

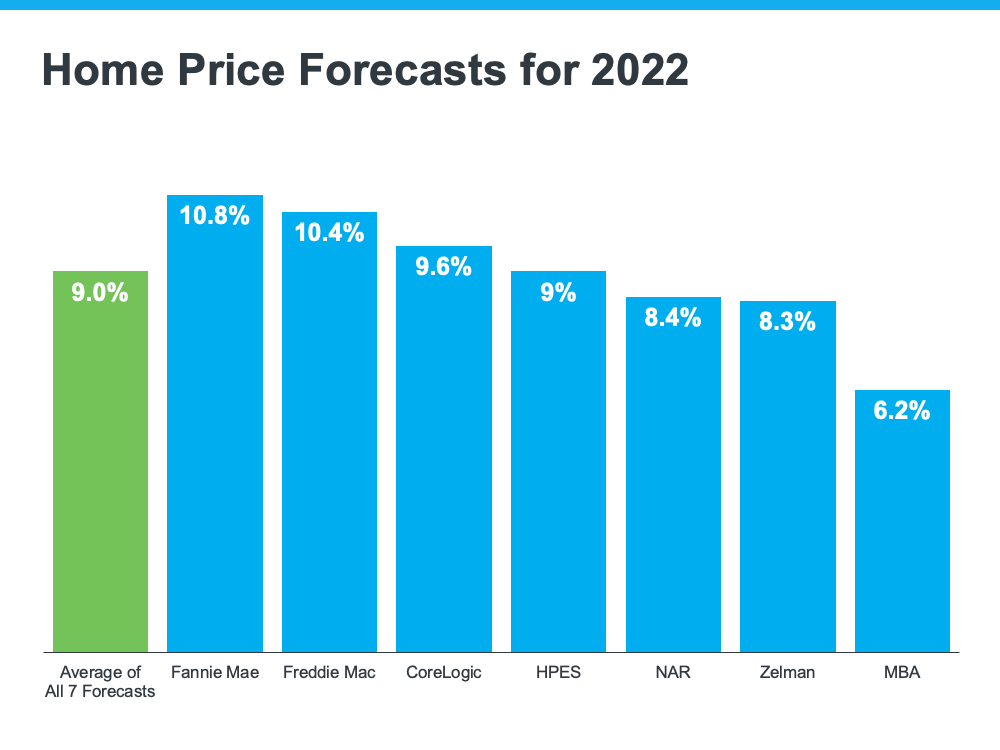

Where Do Experts Say Prices Will Go from Here?

Experts say the housing market isn’t set up for a price decline due to that ongoing imbalance between supply and demand. In the latest home price forecasts for 2022, they’re calling for ongoing appreciation throughout the year (see graph below):

While the experts are forecasting more moderate price appreciation, the 2022 projections show price gains will remain strong throughout this year. First Americanexplains it like this:

“While house price growth is expected to moderate from the rapid pace of 2021, strong home buyer demand against a backdrop of historically tight inventory of homes for sale will likely keep appreciation positive in the coming year.”

What Does That Mean for You?

The biggest takeaway is that none of the experts are projecting depreciation. If you’re a homeowner thinking about selling, the higher price appreciation over the last two years has been great for your home’s value, but it’s also something you should factor in when planning your next steps. If you’ll also be buying a home after selling your current house, you shouldn’t wait for prices to fall. Waiting will only cost you more in the long run because climbing mortgage rates and rising home prices will have an impact on your next home purchase. Freddie Macsays:

“If you’re thinking about waiting until next year and that maybe rates are higher, but you’ll get a deal on prices – well that’s risky. It may be more advantageous to purchase this year relative to waiting until 2023 at this time.”

Bottom Line

If you’re thinking of selling to move up, you shouldn’t wait for prices to fall. Experts say prices will continue to appreciate this year. That means, if you’re ready, buying your next home before prices climb further may make the most financial sense. Let’s connect to begin the process of selling your current home and looking for your next one before prices rise higher.

Why This Housing Market Is Not a Bubble Ready To Pop

Homeownership has become a major element in achieving the American Dream. A recent report from the National Association of Realtors (NAR) finds that over 86% of buyers agree homeownership is still the American Dream.

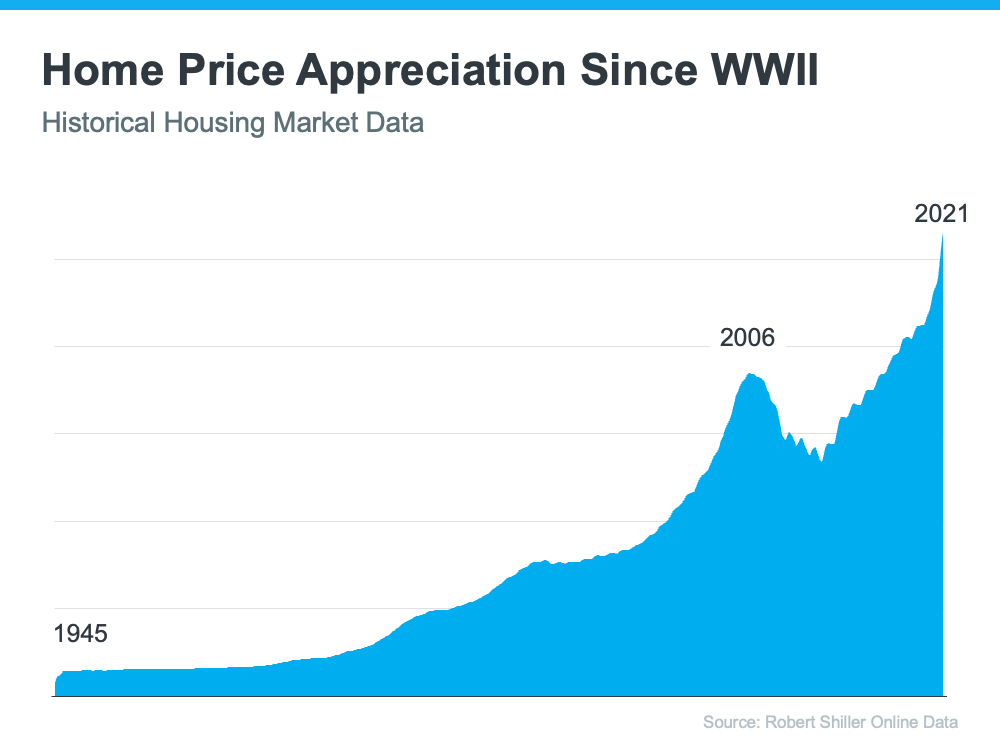

Prior to the 1950s, less than half of the country owned their own home. However, after World War II, many returning veterans used the benefits afforded by the GI Bill to purchase a home. Since then, the percentage of homeowners throughout the country has increased to the current rate of 65.5%. That strong desire for homeownership has kept home values appreciating ever since. The graph below tracks home price appreciation since the end of World War II:

The graph shows the only time home values dropped significantly was during the housing boom and bust of 2006-2008. If you look at how prices spiked prior to 2006, it looks a bit like the current spike in prices over the past two years. That may lead some people to be concerned we’re about to see a similar fall in home values as we did when the bubble burst. To help alleviate those worries, let’s look at what happened last time and what’s happening today.

What Caused the Housing Crash 15 Years Ago?

Back in 2006, foreclosures flooded the market. That drove down home values dramatically. The two main reasons for the flood of foreclosures were:

1. Many purchasers were not truly qualified for the mortgage they obtained, which led to more homes turning into foreclosures.

2. A number of homeowners cashed in the equity on their homes. When prices dropped, they found themselves in an underwater situation (where the home was worth less than the mortgage on the house). Many of these homeowners walked away from their homes, leading to more foreclosures. This lowered neighboring home values even more.

This cycle continued for years.

Why Today’s Real Estate Market Is Different

Here are two reasons today’s market is nothing like the one we experienced 15 years ago.

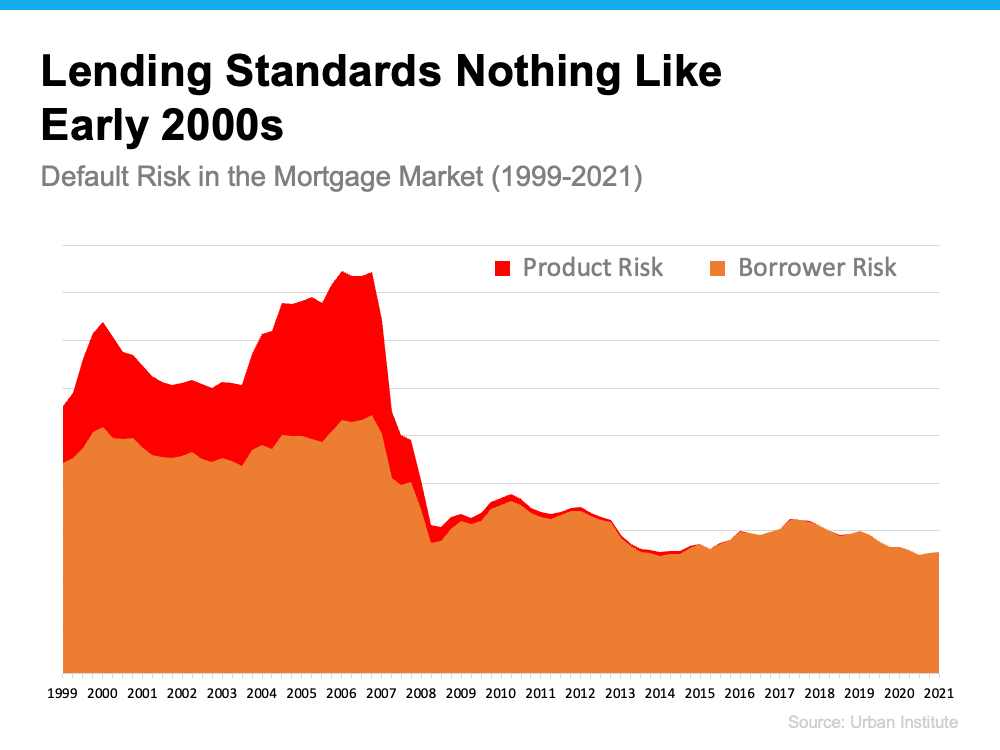

1. Today, Demand for Homeownership Is Real (Not Artificially Generated)

Running up to 2006, banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance their current home. Today, purchasers and those refinancing a home face much higher standards from mortgage companies.

Data from the Urban Institute shows the amount of risk banks were willing to take on then as compared to now.

There’s always risk when a bank loans money. However, leading up to the housing crash 15 years ago, lending institutions took on much greater risks in both the person and the mortgage product offered. That led to mass defaults, foreclosures, and falling prices.

Today, the demand for homeownership is real. It’s generated by a re-evaluation of the importance of home due to a worldwide pandemic. Additionally, lending standards are much stricter in the current lending environment. Purchasers can afford the mortgage they’re taking on, so there’s little concern about possible defaults.

And if you’re worried about the number of people still in forbearance, you should know there’s no risk of that causing an upheaval in the housing market today. There won’t be a flood of foreclosures.

2. People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

As mentioned above, when prices were rapidly escalating in the early 2000s, many thought it would never end. They started to borrow against the equity in their homes to finance new cars, boats, and vacations. When prices started to fall, many of these homeowners were underwater, leading some to abandon their homes. This increased the number of foreclosures.

Homeowners didn’t forget the lessons of the crash as prices skyrocketed over the last few years. Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has more than doubled compared to 2006 ($4.6 trillion to $9.9 trillion).

The latest Homeowner Equity Insights report from CoreLogic reveals that the average homeowner gained $55,300 in home equity over the past year alone. Odeta Kushi, Deputy Chief Economist at First American, reports:

“Homeowners in Q4 2021 had an average of $307,000 in equity – a historic high.”

ATTOM Data Services also reveals that 41.9% of all mortgaged homes have at least 50% equity. These homeowners will not face an underwater situation even if prices dip slightly. Today, homeowners are much more cautious.

Bottom Line

The major reason for the housing crash 15 years ago was a tsunami of foreclosures. With much stricter mortgage standards and a historic level of homeowner equity, the fear of massive foreclosures impacting today’s market is not realistic.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link